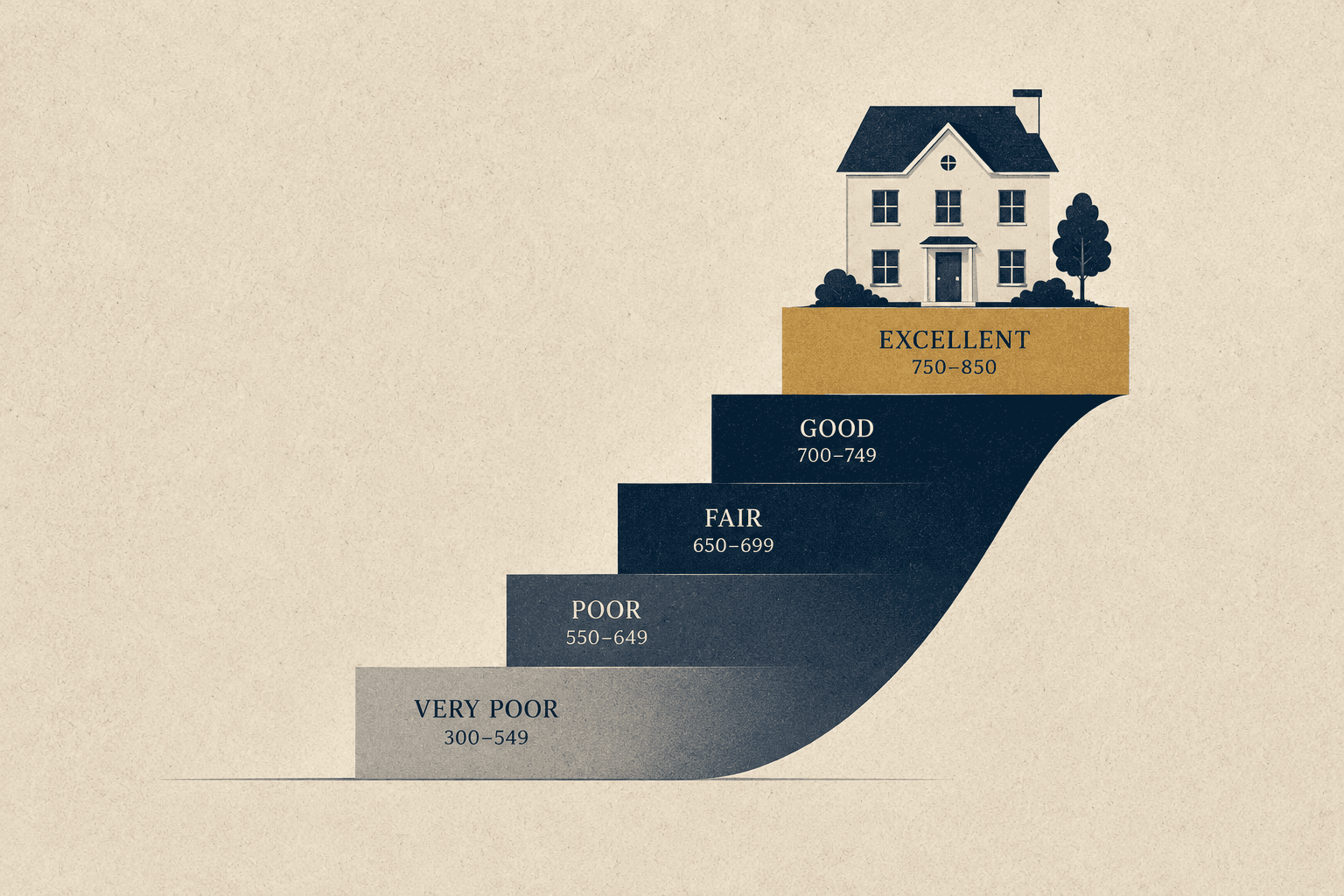

Think of your credit score as a trust rating. A high score tells a lender you pay your bills, so they reward you with a lower interest rate. A lower score makes you look riskier, so they charge you more. That gap may sound small, but spread over a 30-year loan it can add up to tens of thousands of dollars. The good news is that you do not need perfect credit to buy. You just need to know the thresholds, and where yours lands.

The main loan types and the scores they want

There are three common ways to borrow, and each has a different credit bar. Knowing which one fits you tells you the score to aim for:

- Conventional loan: starts around 620, but the best rates kick in at 740 and up.

- FHA loan (designed for lower scores): as low as 580 with 3.5% down, or 500 with 10% down.

- Jumbo loan (for very expensive homes): usually needs 700 to 720 and more savings in the bank.

Why a higher score saves you real money

A better score does more than get you approved. It lowers your rate, and a lower rate means a smaller payment every single month.

Here is a concrete example. On a $600,000 loan, the difference between a 680 score and a 760 score is often about half a percent in rate. That works out to roughly $200 to $300 more per month for the lower score, every month, for years. On top of that, if you put down less than 20%, you have to pay mortgage insurance, and that fee is also cheaper when your score is higher. So the same house quietly costs a weaker-credit buyer much more.

FHA loans: a lower bar, with a trade-off

If your score is in the 500s or low 600s, an FHA loan can get you in the door with as little as 3.5% down. That is a real path to ownership for many first-time buyers.

The trade-off is the insurance. FHA loans require a mortgage insurance fee that, for most borrowers, never goes away on its own, even after you build equity. Many people use an FHA loan to buy now, then refinance into a regular loan later once their score and equity have improved, which drops that fee.

How to raise your score in 60 to 90 days

If your score is not where you want it, you can often move it in a couple of months. The biggest, fastest lever is your credit card balances. Aim to use less than 30% of each card's limit, and under 10% is even better.

A few more proven moves:

- Check all three credit reports and dispute any errors, like a wrong late payment.

- Do not open new credit cards or loans while you are getting ready to buy.

- Ask your lender about a "rapid rescore," which can update your score in days instead of months.

- Do not close your oldest credit card. A long history helps your score, and closing it can actually lower it.